Let a little warm air from the markets? Unless it’s “messy”.

By Wolf Richter for Wolf Street.

It seems a rare sight for the Treasury Secretary and Fed Chair to color-coordinate comments about their growing long-term yields. On Friday, Treasury Secretary Janet Yellen echoed what Fed Chair Jerome Powell said Thursday in an interview with the Wall Street Journal in an interview on PBS Newshor.

When Yellen was asked about the rising long-term yields that the Cribbies on Wall Street are panicking about, Yellen calmly said: “There has been some increase in long-term interest rates, but mainly because I think market participants have a better Recovery, as successful in vaccinating people and a strong fiscal package that is to get people back to work. ”

“Doesn’t rising interest rates worry you?” She was then asked.

“I think they’re a sign that the economy is getting back on track, and market participants see it, and they expect a stronger economy,” Yellen said. “And instead of staying below the level that has been desirable over the last few years, it will start to see inflation come in the normal range of about 2%.” And inflation may be higher than that, but it will be short-lived, he said.

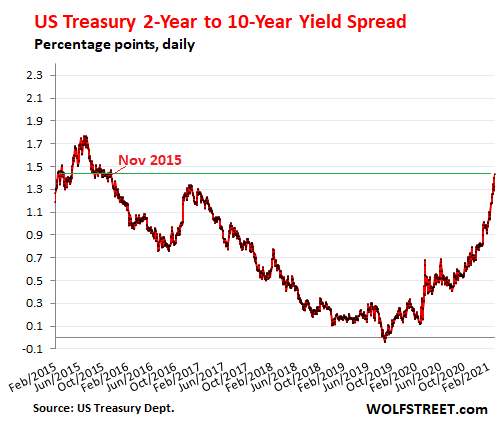

On Friday, the Treasury’s 10-year yield rose to 1.57%, which is still ridiculously low, given the outlook for inflation, and will allow inflation to run above 2% following the Fed’s insistence, as measured by “Core PCE”. Measure that almost always the U.S. The lowest reading of inflation is produced in. But that 1.57% was the highest since February 14, 2020:

The spread between Treasury 2-year yields (0.14%) and 10-year yields (1.57%) widened by 1.43%. By this measure, the yield curve since November 2015 is the highest:

This increase in 10-year yields has caused the Fed to rumble among the Cribbies on Street to do something to bring them down. They have already outlined measures, including another “Operation Operation Twist”, where the Fed sells short-matured Treasury securities and buys long-maturing Treasury securities. This focused purchase of long-standing treasuries will push up their prices and push their yields there.

The Wall Street Crybabies is crying out for this because large amounts of leverage bets on Treasury securities cause huge losses.

Physical rupee serv-tight-sounding Treasury bond funds focused on long maturity are also taking a growing loss. Shares of Eisers 20 Plus Year Treasury Bond ETFs hit a 10-year low in August last August. [TLT] Decreased by 19%.

And the 10-year yield is still 1.57%. Back in November 2018, it more than doubled to 3.24%. In April 2010, there was a day when the 10-year yield fell by more than 4%. Those were the days now! The one we’re talking about now is a modest miniscule 1.57%, and the CryBBs are starting to walk the Fed the wrong way to get rid of this unsatisfactory yield.

The Fed in a unified tone suggests that rising yields are a sign of strength, and as long as they are a sign of rising strength and not a little tight in the financial situation, it will allow them to grow.

It’s funny that Yellen is now equipped up to Powell and sings from the same hymn sheet with Powell to push against the Crybabies on Wall Street.

In an interview with the Wall Street Journal, Powell expressed comfort with higher long-term yields and rising inflation expectations the day after the Fed’s position.

The Fed expects inflation to continue for two reasons, Powell said in an interview. The “base effect” of the fall in the inflation index in spring last year; And “cost increases” that could lead to “obstacles” to the economy reopening, creating “some upward pressure on prices”. But the Fed will remove the “one-time effects” and any “momentary rise in inflation,” and it will become “patient” with the rate hike, he said.

Considering the rising yields on bonds, he said: “I would be concerned about the ever-tightening of the markets by the volatile conditions in the markets or the persistent tightening of the financial situation threatening our achievement of our goals.” The phrase “awkward situations” came up many times.

The extra momentum in long-term yields was “something that was significant and caught my attention,” Powell said. “But again, that’s the wide range of economic conditions we’re looking for, and that’s really the key; That’s a lot of things. We want to see and worry if we don’t see “systematic conditions” in the markets, and we don’t want to see continued tightening in the extended financial situation. It’s really a test, “he said.

Unless conditions are “disorganized”, as long as 10-year yields are “systematically” zigzagged, and go overboard, and as long as “a wide range of financial conditions” are favorable – they are still “very appropriate”. Yes, he said – the Fed will allow long-term yields to do what they can and see them as a sign of economic strength and welcome higher expectations of inflation.

On the other hand, if the markets become volatile again, as they were in March, “the committee is ready to use the tools to achieve its goals,” he said.

He refused to nail down what level of 10-year yields the Fed would panic and start rummaging through its toolbox. But obviously, that point isn’t around the corner yet.

The effect is that long-term higher yields are putting some warm air out of the markets. And the Fed can encourage it, as long as it’s “tidy”.

The bond market has been buzzing for months with long-term crop and investment-grade corporate bonds with huge losses spread across the treasury. The housing market will eventually respond to rising mortgage rates, and mortgage rates began to rise in early January.

But the junk-bond yield has hardly got a surprising record. Demand for this specialty has grown significantly as a result of recent corporate scandals. This enthusiasm for junk bonds – which funds all types of goblin companies to burn their cash – is a sign of “extremely favorable financial position”.

While the average BB yield doubles to 7% and the average CCC yield doubles to 15% (my cheat sheet for bond credit ratings), the financial situation is getting tougher, funding for cash-burning machines is getting tougher and more expensive, And the Fed will panic. But that hasn’t happened yet.

Have fun reading Wolf Street and want to support it? Using ad blocs – why do I get it perfectly – but want to support the site? You can donate. I really appreciate it. Click on a beer and iced tea mug to find out how:

Would you like to be notified by email when Wolf Street publishes a new article? Sign up here.

![]()