[ad_1]

The share price of American electric vehicle maker Tesla (TSLA-US) has repeatedly skyrocketed, CEO Musk’s value has also risen and he has become the second richest person in the world. Taiwanese companies have had a good time. R&D and manufacturing ability in the development of information and communications in the past. Become a niche to enter the Tesla supply chain, and Taiwan factories that have been deployed in advance, with the constant growth of Tesla shipments, are now gradually enjoying the fruits of the profits.

Tesla’s Shanghai Gigafactory is about to begin mass production of the Model Y and has set a goal of reaching a weekly production capacity of 5,000 vehicles by 2021. Tesla also announced that it will implement “local supply” and expand use of locally produced models. Regarding the proportion of components, Taiwanese factories enter the supply chain directly or indirectly, accounting for up to 75%. They mainly focus on the top five areas of battery materials, automotive lenses, automotive semiconductors, automotive electronic components, and the Internet of vehicles.

Among them, the battery, a key component of electric vehicles, is a battlefield for military experts. Major manufacturers such as Panasonic from Japan, Samsung and LG from South Korea, CATL and BYD from China dominate the world. Taiwanese manufacturers can only provide related chemical materials, such as CommScope (4739-TW) and Meiqima (4721-TW), Taiwan’s second largest oxidation catalyst factory, supplied cobalt, nickel and other metallic materials to Panasonic, avoiding with successful Tesla supply chain.

After Tongxin Electronics (6271-TW) CMOS Image Sensor (CIS) Packaging and Testing Plant was formally merged with Shengli in June, Aptina, which is a major customer of Shengli, ON Semi, is the main supplier of Tesla’s CIS, and thus has become a special provider. In the SLA supply chain, in the future, automotive lens pixels will continue to advance to 2 million pixels, and the demand for RW packaging technology will grow substantially, and Tongxindian is expected to benefit directly.

PCB manufacturers Dingying (6251-TW) and Hitech (5439-TW) provide automotive plates for American electric vehicles. Hitech has held onto the new energy vehicle market from the start. Thick copper plates are mainly used in electric vehicle power supplies; Ying covers a wide range, including traditional fuel vehicles and new energy vehicles. Applications include unsecured automotive multimedia, inner tubes, standard and safety tire pressure, engine monitoring, air bags, etc., which account for a large proportion of revenue.

Lianjia (6288-TW), a leading manufacturer of LED car lights, leverages its patented technology and has high visibility of long-term orders. It has already seen 2026. The legal entity estimates that Lianjia’s revenue is expected to maintain double-digit annual growth for at least five years into the future. Heda (1536-TW) is Tesla’s exclusive gearbox supplier. The third quarter has gone from loss to profit. The third factory in Chiayi is still under construction according to the original plan. It is expected to go into operation after the completion of early next year and is ready.In addition to strong customer demand for electric vehicles after 2021, the legal entity expects demand by the end of the year to be strong and development prospects in the long term they are also promising.

After completing the acquisition of Xushen International in April this year, auto parts maker Zhishenke (4551-TW) entered Tesla’s supply chain and supplied the transmission engine cooling system. Since Zhishenke has a high penetration rate for Advantage electric vehicles and hybrid models, the legal entity believes that long-term growth is expected, and the net earnings per share next year is expected to be close to 10 yuan.

Among the Taiwan power supply manufacturers, Delta (2308-TW) is the fastest. Almost all European, Japanese and American automakers are customers. The relevant components of the power supply and charging batteries have been implemented in the car, including the starter and drive motors. Shipments from car chargers, power control centers, etc. are expected to increase next year. Additionally, Kangshu (6282-TW) is also actively deploying electric vehicles. Today, it has received orders from major electric vehicle manufacturers in Japan and the United States. It mainly supplies vehicle starting, charging and bypass systems.

China’s new energy vehicles enter high-speed growth stage and Taiwan factories stagnate in advance

China’s bullish policy has continually promoted new energy vehicles. The industry noted that currently, Chinese automakers rarely order directly from Taiwanese manufacturers. Taiwanese manufacturers have relatively new opportunities because they have joint ventures in China. However, because most automakers are still in the development stage, Taiwanese manufacturers have It difficult to sell goods. However, 2021 will enter a period of rapid growth. The government will actively promote new infrastructure and accelerate the construction of charging piles. During the 14th Five-Year Plan period, the annual production value will be in the hundreds of billions.

In terms of global EV sales last year, Tesla was far ahead, followed by Beiqi, BYD, SAIC, Geely and Beijing’s Guangzhou Automobile. With the pace of China’s new energy promotion policies, they gradually moved away from the “plug-in hybrid”. Moving to “pure electricity”, Weilai, Xiaopeng and Ideal Auto have also received market attention.

The NIO electric vehicle delivery volume hit a new record in the third quarter, with revenue reaching RMB 4,526 million, an annual increase of 146%, which was better than expected. Fourth quarter revenue is estimated to fall between RMB 62.6-6.44 billion, with an annual growth rate of about 119.7% -126%, with the increase in sales prices and manufacturing efficiency, losses have gradually converged .

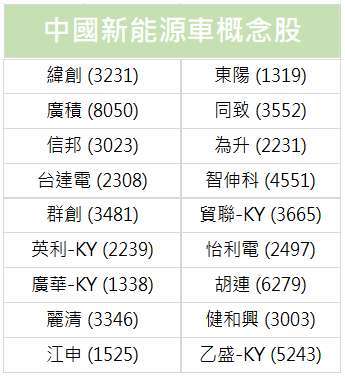

Wistron (3231-TW) has actively entered the electric vehicle market in recent years. In 2014, it invested 600 million yuan in a stake in automotive electronics maker Zongying. It also cooperated with Guangji (8050-TW) to implement the artificial intelligence car computer market. It entered NIO’s supply chain in 2010, exclusively supplying electronic control systems, and Wistron is also one of the shareholders. As NIO shipments increase, operations are expected to benefit directly.

SINBON (3023-TW), a major manufacturer of wiring harnesses, entered the NIO supply chain very early and is the exclusive supplier of charging guns, charging pile harnesses, and laser radar LiDAR harnesses. With the increase in the volume of delivery of NIO, except for vehicles In addition to increasing demand for components, SINBON is expected to benefit from the accelerated deployment of infrastructure such as charging stacks. Delta is also one of NIO’s vehicle charging power supply supply chains and related products. Delta recently revealed that the order for electric vehicle products is complete and the situation of the car factory will gradually improve.

Yingli-KY (2239-TW) has the broadest design in China’s new energy vehicle market, entering NIO, Beiqi New Energy, etc. The revenue share from electric vehicle products is expected to rise from 4% today to 12% next year. Great opportunities for electric vehicles.

In addition, Guanghua-KY (1338-TW), Liqing (3346-TW), Jiangshen (1525-TW) and Dongyang (1319-TW), etc., will subsequently enter the new energy vehicle supply chain through joint ventures. It is worth noting. Legal entities are optimistic about Weisheng (2231-TW), Tongzhi (3552-TW), Zhishenke (4551-TW), Bizlink-KY (3665-TW), Yilidian (2497-TW), Hulian (6279) -TW) and Jianhexing (3003-TW), etc.

[ad_2]