[ad_1]

Before the elections, the US bailout bill will not be too high, reducing the scope for the rally in US stocks in October. Wang Rongxu, an analyst at Wanbao Investment Consulting, estimates that after the November elections, regardless of who is elected Trump or Biden, the bailout will be approved. US stocks, revised in September, bottomed out in October and rose in November. The main issue is low interest rates and helpful policies.

Part of the population will begin to be vaccinated next year and the economy will recover even more than this year. Semiconductors are the top electronic products, and foundry is a leading indicator of downstream and middle business improvement. The Taiwan stock market has risen above all moving averages and there is a risk of ditching the September crash, but the volume is insufficient and the market is not large.

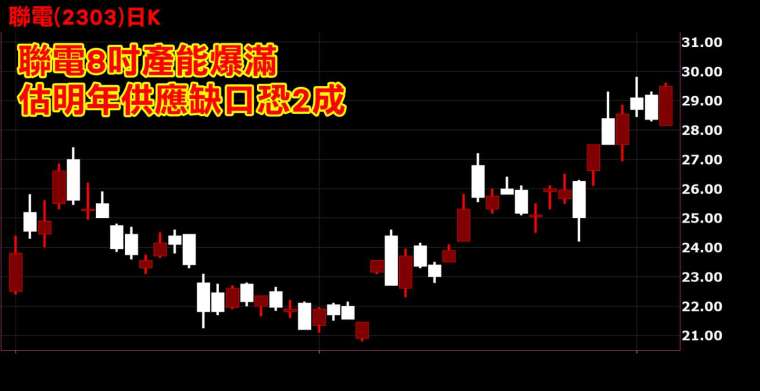

Wang Rongxu, an analyst at Wanbao Investment Consulting, said the market waits and sees the US elections, but yield stocks will first strike back at the market. The 8-inch and 12-inch foundry capacity, which was originally in rush capacity, will be added to the US entity list Major customers have transferred orders. SMIC’s manufacturing process and revenues are similar to UMC (2303-TW). The controller and power management ICs are cast in bulk, making UMC a major beneficiary of SMIC sanctions.

UMC (2303-TW) acquired a 12-inch wafer factory in Japan last year, adding even more to this year’s performance. The share price speaks for itself: TSMC hasn’t broken the previous high this year and UMC has already led the way. Many people have recently wondered, will the UMC go up again? Wang Rongxu, an analyst at Wanbao Investment Consulting, summarized three key points.

First, UMC’s performance in the fourth quarter will not be weak in the off-season. Since the depreciation of new equipment is too high, second-hand equipment cannot be bought with money. Most manufacturers can only eliminate bottlenecks and there is little room to increase capacity. The 8-inch capacity gap will reach 20% and the casting fee is expected to rise further.

Second, UMC’s EPS is estimated to reach 1.6 yuan this year and 2.5 yuan next, and the P / E for this year and next will be about 20 and 12 times respectively. The industry world (5347-TW) estimates that EPS will be 3.7 yuan this year and 4.5 yuan next year, and the P / E ratio will be 26 this year and next. And 21 times, UMC’s P / E ratio is relatively low.

Third, UMC’s net worth per share is 11.64 times, which is not only less than 3.2 times the global wafer casting industry average, but also much lower than 5.9 times. outposts of the world.

By viewing this, you can understand why legal persons continue to buy UMC.

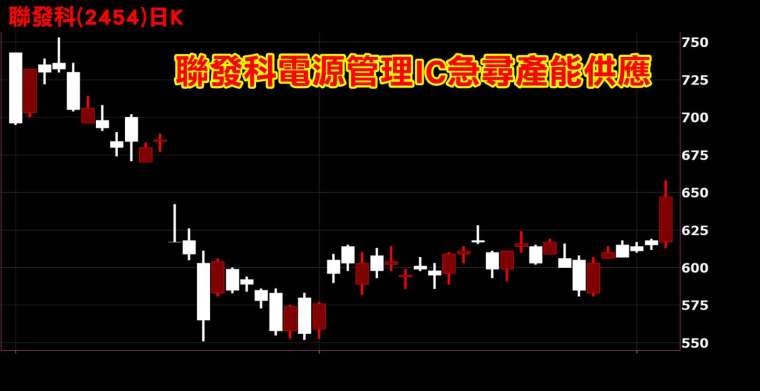

Foundry capacity is full, and even IC design customers’ chip inventory is in a hurry Power management ICs that have always been cast in 8-inch factories are in short supply. Revenues for September Just Announced. Power Management ICs Companies Dazhong (6435-TW), Fuding (8261-TW) and Mota (6138-TW) Have Set New Highs, and Future Product Prices they can also increase.

It should be noted that many people may not have thought that MediaTek (2454-TW) is also a major manufacturer of power management ICs. Although Huawei is sanctioned by the United States, the market share will be transferred to other Chinese brand manufacturers, which has limited impact on MediaTek and its share price has also fallen to reflect Huawei’s bearishness. 10/7 MediaTek broke through with a red bar with volume, and it smelled like the bottom of the middle ground.

Wang Rongxu, an analyst at Wanbao Investment Consulting, said the moment is entering the fourth quarter. In addition to cast IC design, there is a lagging group of semiconductors that is expected to make up for the increase, namely PA power amplifiers.

Affected by Huawei, Winmao (3105-TW) has not increased since this year, but its revenue in the first 9 months reached 18.5 billion, an increase of 28% over the same period last year. Next year, 5G mobile phones will be fully launched. Winmao customers include all brands of mobile phones. Large factories have a high degree of profit.

In addition, Hongjieke (8086-TW) has an even more outstanding performance. In the first nine months, their revenue increased 77% annually. The EPS in the first three quarters is estimated to be more than double that of last year. It mainly benefits from teaching in the remote office, which drives Wi-Fi. Demand for Fi 6. Wi-Fi 6 uses more than twice as much AP as Wi-Fi 5, and home work and classes have gradually become the norm. With the launch of 5G next year, home Internet access broadband traffic will expand. Hongjieke is the second largest GaAs wafer foundry in the world, benefiting from the removal of beautification and gradually increasing its market share in China. US customer Skyworks suffered from a production capacity shortage due to the epidemic, and orders were broken in the fourth quarter, and order momentum continued into the first quarter of next year.

Skyworks is the supplier of the iPhone 12, iPhone 12 will be released next week, Skyworks placed an order with Hongjieke, which is equivalent to letting Hongjieke indirectly catch the iPhone 12 craze.

Wang Rongxu, an analyst at Wanbao Investment Consulting, believes that the estimated volume of Taiwan shares in October has shrunk and there is not much room for the index. Stock selection should return to fundamentals, not just looking for stocks with good September earnings and third-quarter earnings. In the fourth quarter, the revenue momentum should be strong enough to be able to move forward, backward and defend. Analysis of more potential stocks will be shared with readers on Line’s fan club https://line.me/ti/p/@marbo888.

Join the Wang Rongxu fan group for free now and share more information.

YouTube channel of Wang Rongxu, Chief Investor

https://www.youtube.com/channel/UCi-2okN64tcrY5F09E2pb1Q

Wang Rongxu, Head of Investments Shopmaster FB Fan Group

http://bit.ly/2KGYiSg

Wang Rongxu, Chief Investor, Telegram Fan Group

https://t.me/marbo888

The company and individual values recommended for analysis

No inappropriate financial interest ratio Past performance does not guarantee future benefits

Investors must make independent judgments, prudential assessments and their own investment risks.

[ad_2]