[ad_1]

Before the Federal Reserve (Fed) announced its first interest rate resolution this year, US stocks opened lower on Wednesday (27), and the main indices fell more than 1%. Before the deadline, the Dow Jones Industrial Average fell 500 points or 1.7%, the Nasdaq index fell almost 2%, the S&P 500 index fell 1.7% and the rate fell almost 4%.

Among them, the S&P 500 index recorded its biggest drop in 3 months. As risk aversion in the market intensifies, the US 10-year Treasury yield fell below 1%, and the dollar’s one-day rise was the largest since June last year.

According to the financial report, Microsoft (MSFT-US) opened 2% and its earnings and revenue from the Azure cloud exceeded expectations. Boeing (BA-US) fell more than 3% after announcing an annual loss of 12 billion dollars.

Tech heavyweight stocks like Apple (AAPL-US), Tesla (TSLA-US) and Facebook (FB-US) will announce gains later on Wednesday.

On the individual stock news, the frenzied influx of retail investors sent game retailer GameStop (GME-US) soaring 100% at the open on Wednesday, which has soared nearly 700% in the past two weeks. . Cinema chain supplier AMC (AMC-US) also jumped 200% at the opening, and Riley FBR raised its price target for AMC from $ 3.5 to $ 5.5.

The Fed will also announce the first interest rate decision later this year. The current policy is expected to remain unchanged. Investors continue to pay attention to the Fed’s views on the future positive economic situation and the duration of bond buying measures.

The cumulative number of confirmed new crowns in the world surpassed the 100 million mark on Wednesday, causing more than 2 million deaths. Among them, the United States has accumulated more than 25 million confirmed cases and accumulated more than 420,000 deaths, the highest in the country. world.

The Biden administration stated that it plans to order an additional 200 million doses of COVID-19 vaccine from Pfizer and Moderna, bringing the total number of vaccines in the United States to 600 million doses. He also expressed hope that by increasing the amount of vaccine distribution, the vaccination rate can be accelerated. It is expected that the vaccine can be administered to 300 million people in the United States before the end of the summer.

At 22 o’clock on Wednesday (27) Taipei time:

- The Dow Jones Index fell 517.84 points or -1.67%, temporarily reporting 30,027.01 points.

- Nasdaq fell 264.15 points or-1.94%, temporarily reported at 13361.91 points

- The S&P 500 Index fell 63.52 points, or -1.65%, to 3786.10 points temporarily.

- Rates and a half fell 118.93 points or -3.92%, temporarily to 2912.85 points

- TSMC ADR fell 3.03% to US $ 122.81 per share

- Yield on 10-year US Treasuries fell to 1,011%

- New York light crude oil fell 0.19% to $ 52.51 a barrel

- Brent crude oil fell 0.27% to $ 55.76 a barrel

- Gold fell 0.65% to $ 1,838.80 an ounce

- The US dollar index rose 0.49% to 90.590 points

Focus actions:

Boeing (BA-US) fell 2.94% in early trading to $ 196.11.

Boeing announced Wednesday that its fourth-quarter revenue for the fourth quarter of 2020 was $ 15.3 billion, a 15% year-on-year decrease, but was better than Refinitiv’s expectations. The net loss expanded to US $ 8.4 billion and the total annual net loss exceeded US $ 11.9 billion.

AT&T (T-US) fell 2.29% in early trading to $ 29.07.

AT&T reported that its consolidated revenue for the fourth quarter of 2020 fell 2.4% to US $ 45.7 billion, with a net loss of US $ 13.9 billion, or a net loss of US $ 1.95 per share, and a net profit of US $ 2.39 billion on it. last year’s period. EPS reported 33 cents. Not as good as before, but the decline in revenue and earnings was less than market expectations.

Microsoft (MSFT-US) was up 2.19% in early trading to $ 237.41.

Key Figures for the Second Fiscal Quarter of Fiscal Year 2020

- EPS: US $ 2.03, adjusted vs. US $ 1.64 (consensus expectations in Refinitiv survey)

- Revenue: 17% annual increase to US $ 43.08 billion vs. US $ 40.18 billion (consensus expected by Refinitiv survey)

Daily key economic data:

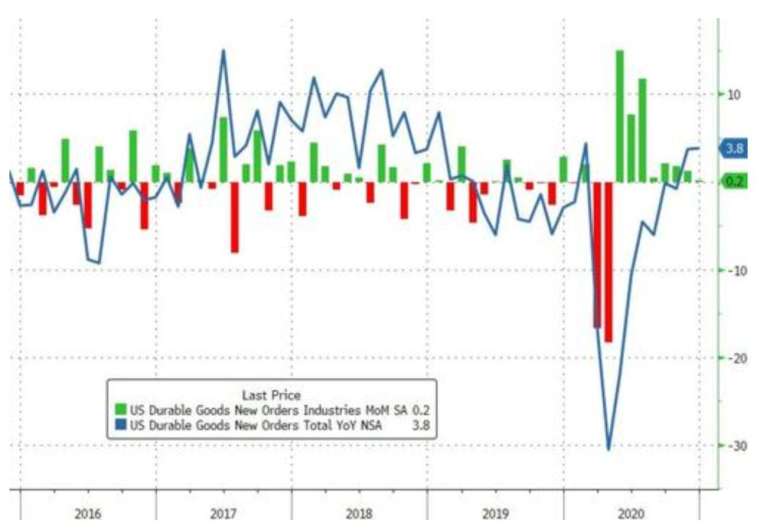

- The initial value of the monthly growth rate of durable goods orders in the United States in December reported 0.2%, 1.0% expected and 1.0% earlier.

Wall Street Analysis:

Deutsche Bank (Deutsche Bank) US economist Matthew Luzzetti believes the interest rate conference will deliver the key message that, from the Fed’s point of view, it is too early to talk about monetary policy normalization and is too early to talk about tightening Fed Ball chairman should send a kind message.

CMC Markets UK market analyst Michael Hewson noted that Raphael Bostic, chairman of the Atlanta Fed, hinted earlier this month that he could scale down bond purchases later this year and raise interest rates sooner. late next year.

Hewson believes that Fed officials must be very cautious not to cause the market to begin to digest the “taper tantrum” situation.

Lou Crandall, an analyst at Wrightson ICAP, predicts that Ball will emphasize the risk of premature action, which is far greater than the risk of delayed action. Crandall also believes that reducing the size of bond purchases has become the key to affecting market sentiment.

[ad_2]