[ad_1]

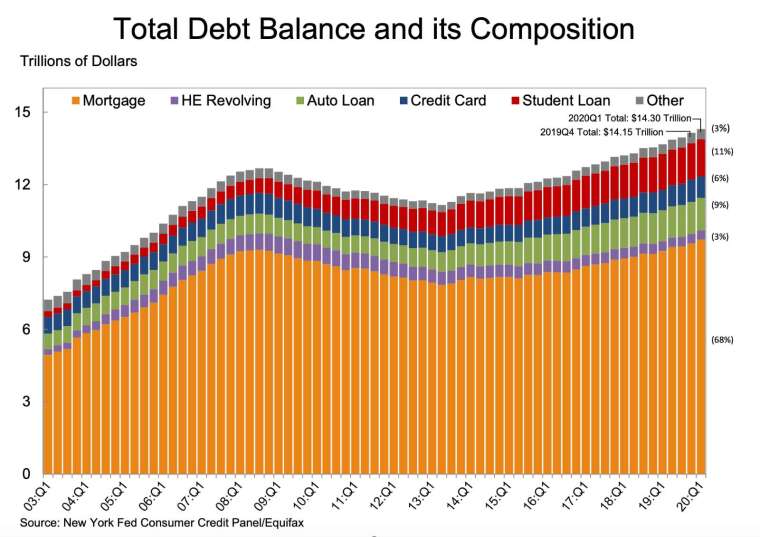

The New York Fed released its latest report on Tuesday (5). In the first quarter of this year, total U.S. household debt reached $ 14.3 trillion, setting a new record, which was an increase of $ 155 billion from the previous quarter. Consumer credit data at the end of March this year cannot fully reflect the potential economic impact of the epidemic.

New York Fed data noted that, compared to the previous quarter, the balance of mortgage loans in the first quarter of this year increased by $ 156 billion to $ 9.71 trillion, most other debts. decreased, and the balance of home equity loans (HELOC) also decreased by $ 4 billion. The balance of the payment reached US $ 3,860.

In addition, the balance of nonresidential loans in the first quarter was almost the same as the previous quarter. Student loans increased by $ 27 billion and auto loans increased by $ 15 billion. Most of the new loans were offset by credit card balances and other loan balances. The balance decreased by $ 39 billion.

As for why the decline in credit card balances is the most significant, the New York Fed analysis believes this may be the first sign of a reduction in consumer spending before the outbreak of the New Crown. However, the researchers say more analysis is needed to determine if these changes are related to the epidemic and will continue to focus on further developments.

After a slight increase in the first quarter, student loan debt now totals $ 1.54 trillion, about 10.8% of debt defaults for 90 days or more, and the overall debt default rate falls to 4.6% .

New York Fed Vice President Andrew Haughwout said the latest report primarily reflects the precursors to the epidemic. Although the decline in credit card loans exceeded expectations, it is still not possible to determine its connection to the epidemic. As the economic situation develops, the central bank will continue to focus on data trends and household assets Balance sheet update.

In addition, the researchers also looked at how households obtain loans based on income. Using zip codes, they found that about 60% of the lowest-income households have credit cards, and almost 80% of the highest-income households have credit cards.

Additionally, the loans available to people in low-income areas are decreasing dramatically. For example, for zip codes, the average adjusted loan for people with total incomes less than $ 45,000 is $ 1,900, or even In some regions, consumers can only get loans of a few hundred dollars. For the regions with the highest incomes, median cardholder loans are $ 14,000. A

[ad_2]