[ad_1]

At the time of bailout negotiations and general election uncertainty, the final round of presidential debates before the elections is about to begin. US stocks rose slightly at the open on Thursday the 22nd. The Dow Jones Industrial Average was up 47 points or 0.2%, the Nasdaq Index was up 0.4%, the S&P 500 Index was up 0.3% and rates they rose 0.2%.

Recently, the news of the bailout negotiations has repeatedly caused volatility in the market. Despite Pelosi’s continued optimism, US President Trump issued a message on Wednesday (21) to criticize the Democratic Party for its unwillingness to commit to the aid bill.

Then all eyes will be on the last US presidential debate on Thursday night (22). Current polls show Biden leading Trump in national polls. It will become the key to reversing Trump’s victory.

Concerns about foreign interference in the US elections also intensified market risk aversion. The director of the National Intelligence Agency, John Ratcliffe, accused Iran and Russia on Wednesday (21) of suspicion of interfering in the US elections by spreading threatening and false emails to voters in an attempt to create chaos before the elections.

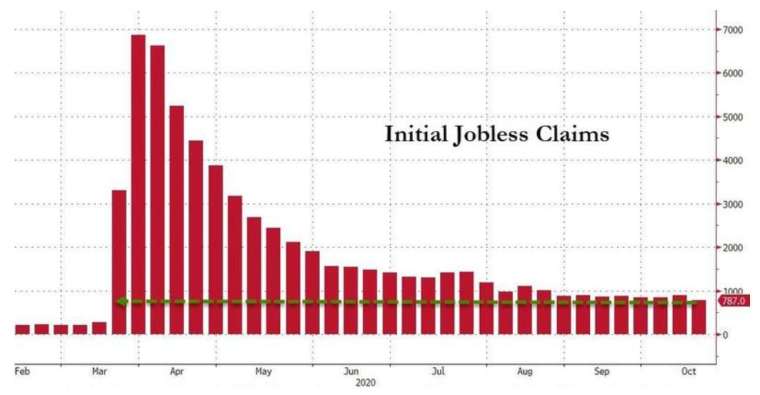

In terms of economic data, the latest data from the US Department of Labor showed that the number of people receiving unemployment benefits fell to 787,000 at the beginning of last week, which was better than expected and the previous value, and fell to the lowest level since the outbreak of the epidemic in March. The number remains between 800,000 and 900,000, and there are signs that the pace of job recovery continues to slow.

At 9 p.m. on Thursday (22) Taipei time:

- The Dow Jones Index rose 47.53 points, or 0.17%, temporarily to 28,258.35 points.

- Nasdaq rose 50.41 points, or 0.44%, to 11,535.11 points temporarily

- The S&P 500 Index rose 9.37 points or 0.27%, temporarily to 3,444.93 points

- Commissions rose 5.32 points and 0.22%, temporarily reporting 2372.57 points

- TSMC ADR rises 0.84% to $ 88.38 per share

- Yield on 10-year US Treasuries increased to 0.821%

- New York light crude oil rose 0.77% to $ 40.34 a barrel

- Brent crude oil rose 0.79% to $ 42.06 a barrel

- Gold fell 1.09% to $ 1,908.40 an ounce

- The US dollar index rose 0.28% to 92.86 points

Focus actions:

Coca-Cola (KO-US) rose 1.31% in early trading to $ 50.65.

Q3 Key facts based on GAAP financial report:

- Net Sales: $ 8.65 billion, a 9% YoY decrease, better than Refinitiv’s forecast of $ 8.36 billion

- Net profit: $ 1.74 billion, a 49% annual decrease

- EPS: 40 cents, 33% annual discount

Q3 Key facts based on non-GAAP financial reports:

- Adjusted EPS: 55 cents, a 2% annual decrease, better than the 46 cents expected by Refinitiv

- Free Cash Flow (FCF): US $ 5.5 billion, a 17% annual decrease

Dow Chemical (DOW-US) was up 3.03% in early trading to $ 50.02.

Q3 Key facts based on GAAP financial report:

- Revenue: $ 9.71 billion, a 10% annual decrease

- Net loss: USD 25 million and net profit of USD 333 million in the same period last year.

- Net loss per share: 4 cents, EPS was 45 cents in the same period last year

Q3 Key facts based on non-GAAP financial reports:

- Adjusted net income was US $ 376 million

- Adjusted EPS: 50 cents, compared to 91 cents in the same period last year, better than the 33 cents expected by Zacks

American Airlines (AAL-US) fell 0.9% to $ 12.63 in early operations.

Q3 Key facts based on GAAP financial report:

- Revenues: US $ 3.17 billion, a 73% annual decrease, better than the US $ 2.81 billion expected by Refinitiv

- Net loss: US $ 2.4 billion and net profit of US $ 425 million in the same period last year

- Net loss per share: $ 4.71, compared to 96 cents a share in the same period last year.

- Daily Cash Consumption: $ 44 million, compared to $ 58 million in the prior quarter. The fourth quarter is expected to drop to $ 25-30 million.

Q3 Key facts based on non-GAAP financial reports:

- Adjusted net loss: $ 2.8 billion

- Adjusted net loss per share: $ 5.54, better than Refinitiv’s estimate of $ 5.86

Daily key economic data:

- In the United States, last week (10/17), the number of initial jobless claims was 787 thousand, which is expected to be 870 thousand, the previous value dropped from 898 thousand to 842 thousand.

- In the United States last week (10/10), the number of people who continued to claim unemployment benefits was 8,373 million, which is expected to be 9,625 million. The previous value was lowered from 10,018 million to 9,397 million.

- At 10:00 p.m. Taipei time, the annualized total number of existing home sales in the United States in September will be announced.

- At 10:00 p.m. Taipei time, the annualized monthly growth rate of US existing home sales will be announced in September, which is expected to be 2.9% and 2.4% sooner.

- At 23:00 Taipei time, the Kansas Fed October Composite Manufacturing Index will be announced, the previous value was 11.0

- At 23:00 Taipei time, the Kansas Fed October Manufacturing Production Index will be announced, the previous value was 18.0

Wall Street Analysis:

Robert Pavlik, chief investment strategist at SlateStone Wealth LLC, said: “The market is still hopeful about the bailout negotiations, but it is increasingly uncertain whether there will be an outcome. Those with practical ideas believe that the new bailout will have to wait until after the general elections. ” It will be released sometime later. “

According to Eleanor Creagh, strategist at Saxo Capital Markets, the market is responding to the political turmoil caused by the rigging of the US elections, as the negotiations have not made any significant progress.

[ad_2]