Will Social Security be for you? Yes, but

By Wolf Richter for Wolf Street.

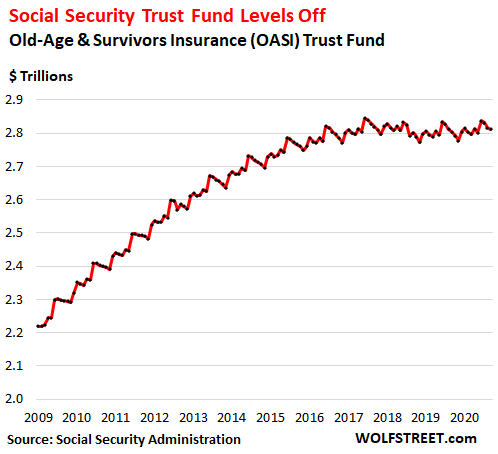

The Social Security Trust Fund – officially the Old-Age & Survivors Insurance (OASI) Trust Fund – closed with a balance of 2. 8 2.81 trillion at the end of September 2020, the second-closest financial year since 2017. An increase of 6. 6.8 billion from a year ago and 10 10 billion from two years ago, according to figures released by the Social Security Administration. After significant growth over the past decade, the Trust Fund has been empty in the same range since 2016.

The balance is seasonal and peaks in June. -L-time peak in June 2017, was 85 2.85 trillion. In June this year, the balance was 84 2.84 trillion. So good:

The Trust Fund invests exclusively in two types of special issue treasury securities: long-term special issue treasury securities with interest of-2.797 trillion and 14 14 billion short-term cash management securities, known as “certificates of credit”. These securities are not traded in public, and therefore their value does not change day by day with the tune of the market. Trust funds buy them at face value, and U.S. The Treasury redeems them at face value.

In contrast, bond mutual funds that have marketable treasury securities should “mark to mark” their treasury on a daily basis (create profit or loss).

By simply investing in treasury securities that the market does not expect, the trust fund pursues the most risky – i.e., least risky – possible strategy.

This setup is an effective, low-cost way to manage trust funds and does not allow Wall Street to load funds with fees and risks. That’s why the Wall Street Trust hates the fund and wants to “privatize” it to get its hands on priv 2.8 trillion dollars, to use it as a dumping ground for fees and risks.

According to the 2020 Trustee Report, 54 million people received Social Security retirement benefits at the end of 2019:

- 48 million retired workers and dependents of retired workers

- 6 million survivors of deceased workers.

The Disability Insurance (DI) Trust Fund is different from the OASI Trust Fund, and is not part of the discussion here. But just to note: in 2019, it benefited 100 million disabled workers and dependents of disabled workers.

During 2019, 178 million people paid social security through payroll taxes. This contribution, along with interest income on securities, yielded Rs 1,062 billion. The total cost of the program was 1, 1,059 billion. A surplus of $ 3 billion. Which was for fiscal year 2019.

The Financial 2020 Trustee Report – 2021 Trustee Report – is not yet available, but we do know that the Trust Fund has increased by 8 6.8 billion this year. So far so good.

Three issues: demographics, Fed interest-rate suppression and inflation.

Demographic

So far, trust funds have entered employees for thousands of years and are benefiting from the earning power they gain as they move forward in their jobs. But there are also pulls on Boomers ’funds that are now between 55 and 75 and are transitioning to the largest number ever in retirement. Over the last few years, this equation has been in balance – both millennials and boomers have huge pay generations. But it will change gradually, and when it does, it will appear as a slide down the line to the chart above.

Fed interest rate suppression.

The effective interest rates earned by securities in trust funds have been declining over the years, especially after the financial crisis, when the Fed uses QE to push long-term interest rates. And the Fed’s current interest rate suppression will show low interest income in future years.

In September, the average interest rate earned on securities was 2.53%, higher than current Treasury yields, thanks to long-term securities that carry higher interest rates on the euro. But since 2009, it has dropped by almost half. And on current interest rate policies, declines will continue.

Trust funds grew 27% in 2009 from 2. 2.22 trillion in September to 8 2.81 trillion in September 2020, with interest income down 30% over the same period.

Beware of Visis Dog: Inflation is higher than COLAs.

The monthly social security payment is adjusted by the annual “Cost of Living Adjustments” for inflation. These annual adjustments are based on the formula that uses the “Consumer Price Index (CPI-W) for all urban wage earners and clerical workers” in July, August, August and September. The Bureau of Labor Statistics will release the CPI on October 13. Cola for 2021 will be set after that. So, just guess here, based on the CPI-W (0.96%) in July and August (1.40%), and in recent months which has been the way forward, this CAOL adjustment for 2021 could be in the range of 1.3%.

The cost of living to retire – or indeed for anyone – will grow very quickly, depending on where they live, how they live, and where they spend most of their money. You are talking about a serious deterioration in the purchasing power of social security payments, even if the cost of living increases by only 1 percent faster than the annual CAO each year after 10 years, 20 years or even 30 years. Inflation will eat up more than retirees’ lunch.

Efforts to make inflation more risky.

Discussions are underway to shift from COPI-W to chain-type price index because They run lower than CPI-W, and so a small increase in inflation each year eats up more in the purchasing power of social security payments.

One can rarely snatch through Social Security, and use their savings – if they have one – to supplement their budget. But every year, this gets harder, and this retiree has to be cut, and cut back, and cut year after year. Whenever this shift in the chain-type index for CLAS occurs in Congress, the voices of everyone, young and old, should be lowered, as it would undermine social security as a security measure.

So, Social Security will be for you, but

You can rely on social security payments. But they will lose purchasing power. The purchasing power of payments will decrease every year, year after year, as the CLA is not enough to cover the actual increase in the cost of living.

This is just a simple fact, and it is no accident, it is purposely built into the system. And this reduction in purchasing power can shave 20% or 30% of your standard of living from the first 20 years before retirement. If initially it was difficult to live on social security, it would be ruthless after 20 years. And people need to add this to their calculations.

Trust Fund Hypothesis Depreciation.

If demographic matters move in the wrong direction, and if interest rate repression continues, eventually the trust fund will pay more than it receives each year in contributions and interest income, and the balance will begin to decline. And if no adjustment is made to contributions or payments, and if the demographic shift continues, at some point, the trust fund will run out. The trustees estimate that the trust fund will run out in 2034 unless some changes are made.

Depreciation of trust funds does not mean that Social Security will deteriorate or “break down” or whatever. It simply means that workers will have to pay a little more, or benefits will be deducted, or both. Social security has been determined before. Increasing the maximum amount of earnings subject to social security tax would be one way, and this has happened before. And there are other ways. These adjustments will be made – as they have been in the past – before the expiration date.

The story of the man who told me that Social Security would collapse before it drew on him.

Over the decades, I have heard many predictions about the promotion of social security. But here’s what I will never forget because I was at an impressive age. When I was a high school senior, my girlfriend’s dad told me that Social Security is a “scam” and it would blow up before he ever used it. He was a CPA and had an accounting and tax firm. After collecting Social Security every month during retirement, he passed away a few years ago. And now his wife is collecting the remaining benefits of his Social Security. Social Security brought it to life, and it will surpass even me.

But Social Security was never intended to provide adequate retirement on its own. My solution is to keep money aside while working, and work as long as possible – past retirement age, especially if you have something interesting. Take a look at all these old politicians: they are all fired, they are exploding, and they do not allow so much fun, not even from income, until someone kicks them. And I intend to do that too – my evil Wolf Straight Media will continue to blast the Mughal Empire until my brain freezes.

After the last crisis, ignited by incredibly cheap money, they are taking the financing of the housing market to the next level. Reading The big boys are back: the financing of single-family homes

Have fun reading Wolf Street and want to support it? Using ad blogs – why do I get it perfectly – but want to support the site? You can donate. I really appreciate it. Click on a beer and iced tea mug to find out how:

Would you like to be notified by email when Wolf Street publishes a new article? Sign up here.

![]()