Consumers are reluctant to apply for credit cards, and the Fed is not happy.

By Wolf Richter for Wolf Street.

Customers of the overall backpack on credit card applications due to the epidemic; And on credit cards they backed up even before they asked for a higher credit limit. And a large percentage of those who applied for a credit card or for a higher credit limit were rejected. Some of the findings from the New York Fed’s Consumer Expectations Survey “Credit Access Survey” are published today. The Credit Access Survey is conducted three times a year (even in February and June).

The notion that consumers are cutting back on credit-card borrowing fades; In the near zero interest rate environment more than 20% of the sky interest rates are where banks make extraordinary profits. And consumers, who can at least afford it, are paying for the bank’s profits from this money.

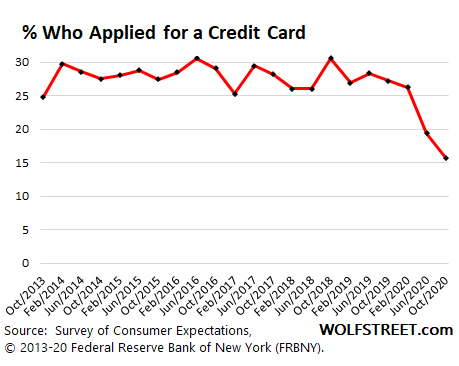

Only 15.7% of consumers said they applied for a credit card in the last 12 months, down from 25% to 31% before the epidemic, and down to 26.3% in February, the lowest ever figure in the survey. From 2013:

The New York Fed, which, like all 12 Federal Reserve Banks, owns the largest financial institutions in its district, laments: “The latest credit access survey shows a strong epidemic on consumer credit markets.”

Consumers are also reluctant to apply for auto loans, but the survey found only one child compared to the cut in credit card application.

And only 7.1% of customers requested higher credit limits on credit cards they already had, the lowest in survey data and down in the range of 8% to 15% in previous years.

So there’s clearly an issue about consumers not coming into the Fed’s line. One reason could also be that credit card interest remains very high, as the Fed is engaged in a historic interest rate crackdown that clears savers and treasury securities holders who can offer no interest on their funds.

Borrowing 10%, 20%, 25% or God 30% – credit card issuers have no qualms about going there – in this low-interest environment, prospects should be super-consumers, or, just good customers in the eyes of the Fed, their hard- Transfer the earned dollars to the banks in the form of interest.

But among those who applied for a credit card, probably to please the Fed, 21.3% declined, the third-highest rejection rate in the data series:

And.1 37.1% who requested a higher credit limit were denied:

These rejection rates suggest a combination of two things: a shift to a mix of requests for customers with a large debt burden and an eFire credit history, while other customers are not applying, there will be an increase in the overall rejection rate; And strict underwriting from banks.

These findings from consumers who backplane on credit cards are another part of the puzzle of why credit card balance has plunged into a historically historic and nerve-wracking way for the Fed.

Credit Credit card balances and other revolving credit balances fell 10.3% year-on-year in October, the largest year-on-year decline in data back in the early days of credit card decline to 9 943 billion (seasonally adjusted, red line), inflation and population growth Despite being 13 years old, August August 2007 saw a balance for the first time:

During the financial crisis, when the credit card balance fell on a seasonal basis (above the green line) from June 2008 to May 2011, another major factor played a role: write-offs by offenders and subsequent lenders. Consumers defaulted heavily on their credit cards – in 2009, almost 14% of all credit card balances were offended – and many went to great lengths to get out of debt.

But that is not happening now. New and unsustainable credit card balances sank into the second and third quarters, powered by a combination of extended-and-predefined deferral programs and stimulus money:

What we are witnessing are the bizarre effects of the extended-and-extend wave of epidemic stimuli. And in the minds of customers right now – I doubt it – borrowing 10% or 20% in a near zero interest rate environment is only good for bank stockholders, and if not, it’s a stupid deal, and that’s it. It is time to starve the banks of that big fat source of revenue by paying interest.

Stimulation sets fatigue. Second consecutive retail sales decline. But sales found a new record in online sales, if not rarely. Reading ... Where the Americans splurged and where they cut back into 13 whiplash-charts

Have fun reading Wolf Street and want to support it? Using ad blocs – why do I get it perfectly – but want to support the site? You can donate. I really appreciate it. Click on a beer and iced tea mug to find out how:

Would you like to be notified by email when Wolf Street publishes a new article? Sign up here.

![]()