[ad_1]

For the first time in history, oil prices hit negative levels in New York earlier this week. In other words, buyers were forced to pay merchants to dump raw materials that they will not be able to remove in May. The devastating effect of the Covid-19 pandemic is the background to what happened on Monday, and there is an imbalance between oversupply and declining demand.

But there are technical aspects that result from the way the US industry works, which is heavily deregulated and highly interconnected with the financial futures (derivatives) market, which also contributed to the “irrational world” in which we also live in this sector. , as António Costa e Silva, former president of Partex and specialist in petroleum geostrategy, explained to the Observer.

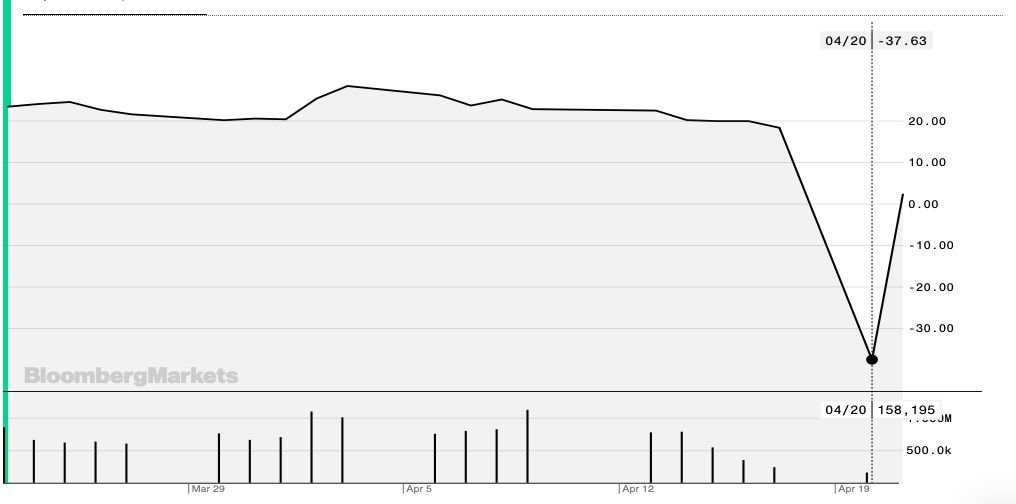

On Monday, the price of a barrel of West Texas Intermediate (WTI), the crude that serves as a benchmark for the US market, fell by more than $ 50 and reached negative $ 37 at 15:15 local time (20:15 in the mainland of Portugal)) In other words, the producers even had to pay $ 37 to anyone who could keep a barrel of WTI to store. At the end of this Tuesday, prices recovered to the most normal, but still $ 10 per barrel. London Brent fell sharply (27%) to less than $ 20.

WTI quote. Source: Bloomberg

What caused the panic on Monday was that it was the last day to deliver the oil sold under futures contracts for the month of May. Producers and traders are required to comply with the amounts provided in these futures contracts (in which the physical delivery of the product takes place after the transaction) that are traded on the stock exchange and there are severe penalties for those who do not make. Not having oil for traditional customers, refineries (also without demand), buyers had to pay to store the product. And they paid record amounts.

Industry expert António Costa e Silva points out that the US regulator still tried to cancel these clauses of futures contracts, to avoid this situation. But “Regulators have little strength in the US market.”

WTI (West Texas Intermediate) is not the crude that serves as a reference for Portugal. Brent is the benchmark oil in Europe and although negative stocks were trading in the United States, London prices closed at $ 25 a barrel on Monday. Although there is a strong historical correlation between the evolution of the prices of these two indices, António Costa Silva says that the development of the industry ‘shale gas‘ It is ‘oil shale oil‘In the United States, initially only consumed in the country, caused the fall in the prices of the product marketed in New York and adopt a different trajectory from the “European brother” (the so-called decoupling).

Incidentally, this relative autonomy was seen again this Tuesday, when prices recovered on the other side of the Atlantic, at values of around six dollars per barrel, and fell sharply on this side, more than 7% to minus $ 20. per barrel. AND It will be this movement that can reach the price of fuel in Portugal.

António Comprido, general secretary of the Association of Oil Companies (APETRO), explains that, “obviously, the fall in the price of the United States will eventually influence the prices of other reference values,” such as Brent. But it is not clear how. Especially since the situation in the USA. USA It has very specific contours: “There has always been a typical problem in the US, which is its ability to get rid of production due to a bottleneck in the refined apparatus,” hence the increase in stocks.

This impact will reach prices, as has happened in the last three months: diesel fell by 22 cents per liter and gasoline by 28 cents, but highly cushioned due to the high weight of the tax burden final prices

The news that the country’s main refinery, Sines, halts production for a month, after the same thing happened in Matosinhos, was known the same day that the price of oil in New York went to negative values. There is no direct relationship between the two realities, but they result from the same structural framework that is cornering the oil companies and the oil market: lack of capacity to store oil or refined products that do not sell, because economies stagnate and companies and people consume much less of everything, including fuels.