[ad_1]

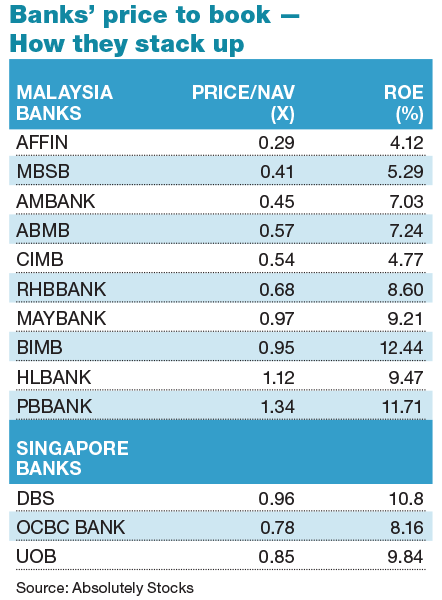

KUALA LUMPUR (September 29): Eight out of 10 Malaysian banks are trading below their book values.

Based on yesterday’s close of RM1.40, Affin Bank Bhd was trading the lowest in terms of price-to-book (P / BV) ratio. The country’s smallest lender was trading at 0.29 times P / BV, followed by Malaysia Building Society Bhd (MBSB) at 0.41 times.

Malayan Banking Bhd was trading 0.97 times, while CIMB Group Holdings Bhd was trading 0.54 times. (See table)

CGS-CIMB Research noted that yesterday banks were trading at their lowest price-to-earnings (PER) ratios since 2013 and were at the lowest P / BV of all time.

“Banks underperformed KLCI by 5.6% in 2019 and 15% [year to date]. The banking sector is currently trading at an attractive forecast P / BV of just one time for the year 2020.

“The [calendar year 2021 forecast (CY21F) PER of 10.5 times] was also the lowest since February 2013. This suggests that the market has appreciated concerns about earnings risks, but has yet to fully appreciate the projected earnings recovery in 2021 as Malaysia recovers from the Covid-19 outbreak. “CGS-CIMB Research said in its latest industry report dated September 19.

Bank valuations appear to be attractive in terms of P / BV, but they are not as attractive in terms of return on equity.

Chan Jit Hoong, a banking analyst at Hong Leong Investment Bank Research (HLIB Research), believes that current valuations of bank stocks are “fair compared to the generation of low ROE (return on equity) banks.”

The average ROE of Malaysian banks is 7% compared to the five-year average of 10%.

“ROE is depressed, but we expect a recovery next year, supported by the recovery of V-shaped earnings,” he told The Edge.

However, Chan cautioned that with recent Covid-19 cases on the rise, there is a risk of a U- or W-shaped profit recovery.

“Also, the unemployment rate [was] still raised to 4.7% [for July] from the normal execution rate of the 3% range.

“As such, I prefer to observe first before becoming more optimistic in the sector. The on-the-spot checks with the banks show that they themselves are also quite cautious and on guard,” said Chan, who has a “neutral” call. in the sector.

He noted that while loan applications continued to increase 5.9% year-on-year in July due to better demand for credit from households (+ 15.4%), credit approvals fell 14.3% due to the restriction of loans for both households (-7.8%) and companies. sector (-22.6%).

However, Chan expects the pressure on banks’ margins to improve next year.

“The pressure from the NIM (net interest margin) should be diminishing, as banks would change the price of their deposits downwards. With deposits revalued downwards and minimal risk to the downside for the OPR (policy rate to one day), the NIMs should improve next year. As of now, there are few downsides, “He noted.

“Despite the increase in Covid-19 cases, recovery is on the way if you look at GDP (gross domestic product) patterns, as the second quarter is probably the worst and the lowest. Also, with the procedures. Appropriate standard operating systems (SOPs) in place now have a better handle on the Covid-19 situation and at the same time the economy can continue to function, “he added.

Chan anticipates that the sector’s gross impaired loan ratio will remain low for the rest of the year, as banks will provide targeted assistance once the general loan moratorium ends this Wednesday (September 30).

However, Chan warned that it can hide real damages and cause a delay in the formation of delinquent loans if the situation does not improve quickly or if the arrival of the second wave of Covid-19 paralyzes the country again.

For the presentation, Chan said the only bank he likes right now is RHB, given its attractive risk-reward profile, supported by undemanding valuations, a strong CET1 ratio of 16.6% (sector: 14.4%), and a fairly large untapped FVOCI (fair value through other comprehensive income). ) Bookings.

HLIB Research has a “buy” call on RHB with a price target of RM5.80.

Meanwhile, CGS-CIMB Research believes large-cap banks with better asset qualities are likely to lead the banking sector downgrading as investors rotate into sectors that are seen as likely to benefit from the projected economic recovery in 2021. .

CGS-CIMB Research noted that it likes Public Bank Bhd and Hong Leong Bank Bhd for their strong asset qualities, RHB Bank Bhd for the fee income driver from the new bancatakaful deal and AMMB Holdings Bhd for attractive valuations (CY21F PER of 6.4 times ).

[ad_2]