[ad_1]

(Oct 16): When it comes to what type of central bank policy is best for attracting foreign investors to Asia during the Covid-19 pandemic, orthodoxy is without question winning.

Let’s take the respective destinations of Indonesia and Malaysia.

Indonesia’s share of debt held by foreigners has dropped to 27% from 39% at the end of last year, while in Malaysia it rose to 24% from a low of 21.7% in April. The difference has narrowed to just 3 percentage points from 14 percentage points at the end of 2019. It’s the same story for cash flows. Indonesia has had net external outflows of $ 6.8 billion this year, while Malaysia has recorded inflows of $ 1.3 billion.

One of the factors that deterred flows to Indonesia has been the central bank’s debt monetization program, in which it buys bonds directly from the government. Money managers worry the plan will take hold, despite repeated assurances to the contrary from the central bank governor and the finance minister. Malaysia’s central bank has stuck to orthodox measures in its efforts to combat the coronavirus – cutting rates and reducing the proportion of legal requirements.

Another factor attracting global funds to Malaysia rather than Indonesia has been Bank Negara’s more aggressive rate action. Malaysian policy makers have cut their benchmark by 125 basis points combined this year, while Indonesia’s has only cut 100 basis points, even though its higher nominal rate means it has relatively more margin.

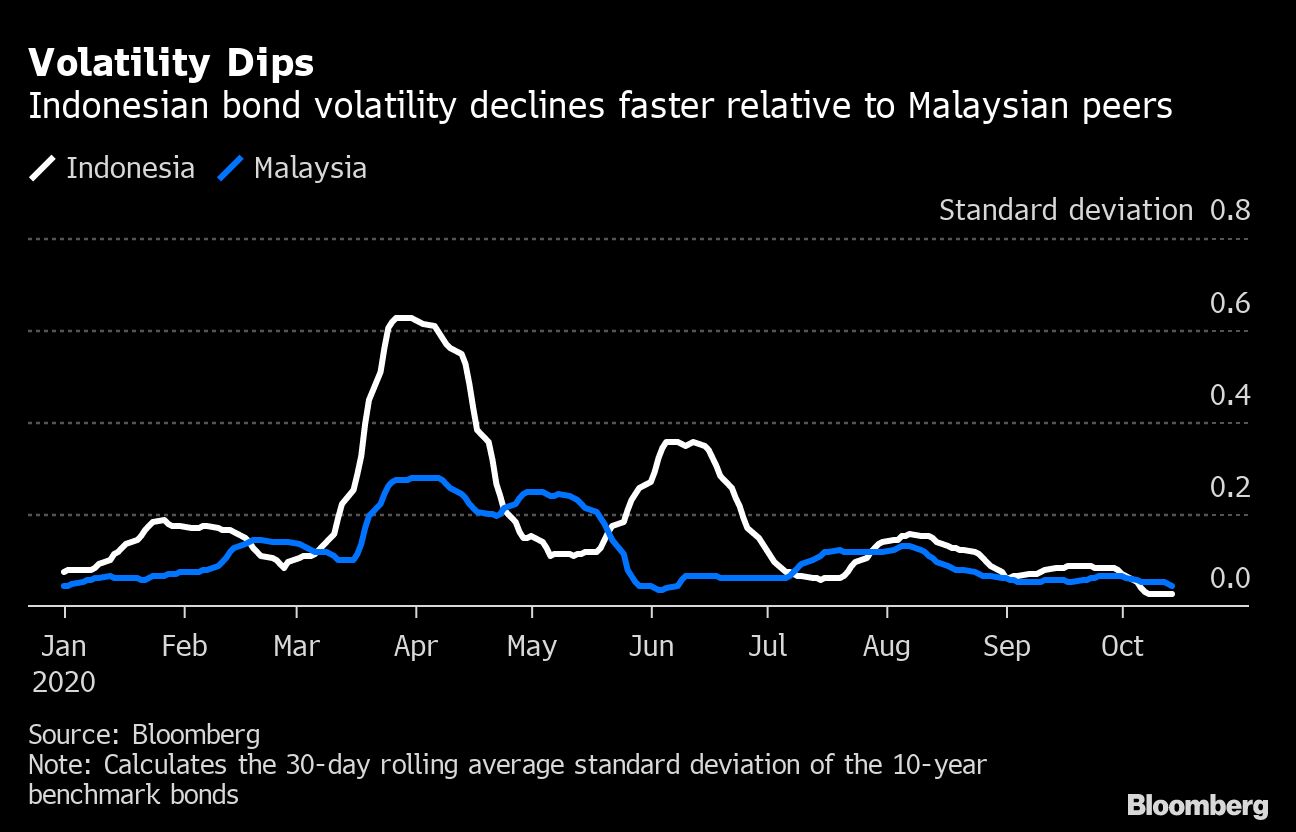

Disappearance of volatility

An important consequence of the change in the cash flow pattern has been to reduce volatility in the Indonesian bond market.

A 30-day moving measure of the standard deviation of Indonesian yields peaked at more than 0.6 in March, while in Malaysia the same indicator stood at 0.3. That indicator of volatility in Indonesia has since fallen to a low of 0.03, below Malaysia’s.

While much of the volatility drop is due to the withdrawal of foreign funds, another factor is the growing presence of Bank Indonesia.

The central bank’s ownership of the nation’s sovereign bonds increased to about 20% as of October 12 from less than 10% earlier in the year, according to Jennifer Kusuma, senior rate strategist at Australia & New Zealand Banking Group Ltd in Singapore. By contrast, Bank Negara Malaysia held 2.6% of the market at the end of September, up from 0.5% at the beginning of 2020, it said.

While foreigners have reduced holdings of Indonesia’s debt, the drop in volatility appears to offer some incentive for potential investors. If volatility remains at current levels, buyers have the opportunity to earn some of the highest real returns in the region with potentially less risk.

What to see

- The Philippines will release the balance of payments figure on Monday and sell five-year bonds the next day.

- Malaysia to announce inflation data on Wednesday

- Thailand will auction 10 billion baht ($ 320 million) of benchmark 2029 bonds (LB29DA) on Wednesday. The previous sale of the same security in September generated an offer to hedge ratio of 4 times. The nation will release customs trade data on Thursday

Note: Marcus Wong is an emerging markets macrostrategist writing for Bloomberg. The comments you make are your own and are not intended to be investment advice.

[ad_2]