[ad_1]

The Ant Financial mascot is displayed in the lobby of the company’s headquarters in Hangzhou in 2019.

Photographer: Qilai Shen / Bloomberg

Photographer: Qilai Shen / Bloomberg

Billionaire Jack Mas Ant Group is poised to carry out what could be the largest initial public offering in history by simultaneously listing in Hong Kong and Shanghai. It is said that it seeks a valuation of $ 225 billion, making it the fourth largest finance company in the world.

A 2011 offshoot of Chinese giant Alibaba Group Holding Ltd., the company has defined and dominates the Chinese payments market through its ubiquitous Alipay app. It also manages the giant money market fund Yu’ebao and the Huabei and Jiebei consumer loan units.

Headquartered in Hangzhou, a sprawling metropolis south of Shanghai, its ambitions go far beyond finance. Here is a thumbnail view of the business units and the challenges the company faces.

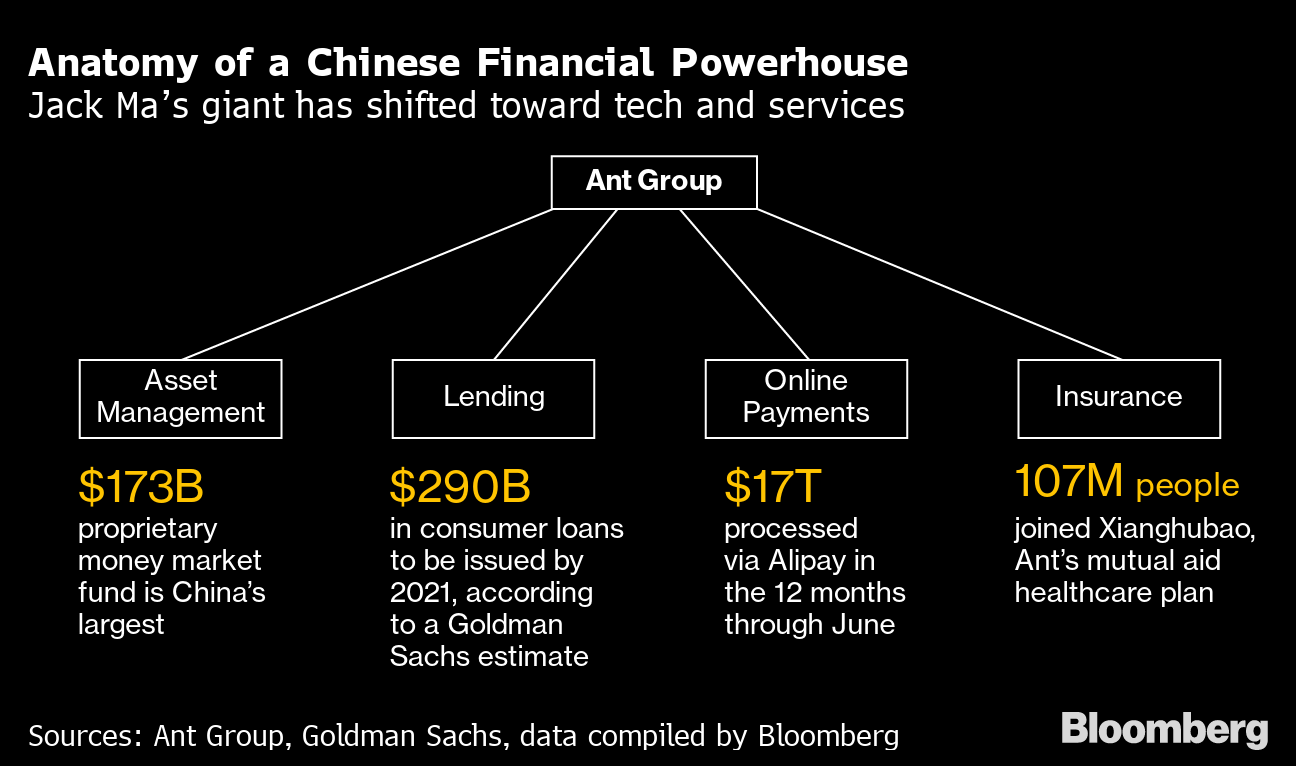

Alipay: a $ 17 billion machine

The world’s largest digital payment platform was created in 2004 as an escrow service for Alibaba to secure transactions on the e-commerce site. For consumers who are wary of online payments, the service was a success and quickly spread to other platforms.

The mobile version, launched in 2009, once had 75% of the market, but has seen its share drop to roughly 55% in competition with WeChat Pay from Tencent Holdings Ltd.

Alipay has 711 million active users, mainly in China, who take advantage of it to buy everything from a quick coffee to a property, generating $ 17 billion in payments in the 12 months to June. But it is also less and less important to Ant, contributing 36% of its revenue in the first half of this year, up from more than 50% just two years ago.

Losing ground in the payment market was one of the reasons why Ant canceled a previous plan for an IPO as early as 2017, people familiar at the time said. Now it is a much more diversified company.

Huabei and Jiebei: a loan party

For those who do not have cash available to spend through Alipay, Ant operates services that make small unsecured loans: Huabei (Just Spend) and Jiebei (Just Lend). The former focuses on quick consumer loans for the purchase of iPhones and refrigerators, while the latter finances everything from travel to education.

Ant uses part of his capital for these loans, but most of the money comes from the banks, and the company acts as a gateway. The platforms made loans to approximately 500 million people in the 12 months to June, charging annualized rates on their smallest loans of around 15%. Its loans could grow to nearly 2 trillion yuan by 2021, according to Goldman Sachs Group Inc.

The firm’s CreditTech business, which includes Huabei and Jiebei, is its largest revenue generator, contributing 39% of the total in the first six months of the year.

The company is now applying for a license to establish a consumer finance company. The new entity would increase Ant’s creditworthiness, as consumer finance companies can lend 10 times their capital, far outpacing the two to three times leverage of Ant’s existing microcredit companies.

Anatomy of a Chinese financial powerhouse

Jack Ma’s giant has been geared towards technology and services

Sources: Ant Group, Goldman Sachs, data compiled by Bloomberg

Yu’ebao: the great stash

With hundreds of millions flocking to Alipay, Ant in 2013 created a money market fund that allowed people to earn interest on the cash they parked in the app, investing as little as 1 yuan. Tianhong Yu’e Bao Money Market Fund is one of the world’s largest of its kind with approximately $ 173 billion in assets. But it has regressed since its heyday after regulators stepped in to limit the amount that each investor can put into the fund.

In 2018, Ant opened the platform to third parties. Now offers fund options from 20+ asset managers. Has partnered with companies including Invesco Ltd., which has seen a fund grow 300 to 400 times its size in March. This year, Ant partnered with Vanguard Group will offer a theft advisor to allow the US giant to advance in China.

Yu’ebao’s unit in Ant accounted for 15% of revenue this year, which has not changed in the last three years.

Credit score

Taking advantage of the wealth of data it is gaining on borrowing and spending patterns, Ant started a credit rating service in 2015 called Zhima Credit. If users opt for the service, Ant performs transaction history checks and also uses data from third-party providers to verify creditworthiness. Ant charges a fee to companies that take advantage of the service, and if customers score high enough, they can avoid paying deposits on everything from renting a bike or booking a room at hotels like Marriott.

Xianghubao: insurance for pennies

Many ants form a powerful colony. In 2019, the company entered the insurance market and created a healthcare product called Xianghubao that allows people to pay a small monthly fee that is bundled together to help cover the treatment costs of members affected by diseases such as cancer, Alzheimer’s and even Ebola.

Ant’s Insuretech unit also sells insurance premiums from third-party companies, and takes a cut. The unit’s revenue increased 47% to 6 billion yuan in the first half, representing 8% of total sales.

Rising Star

Ant Group to Join Top Echelon of Global Financial Firms After Mega IPO

Source: Bloomberg

Global headwinds

Ant had big plans for the United States, but now they have been frozen due to increasing trade and political tensions between the world’s two superpowers. Ma in 2018 gave up on her promise to create 1 million jobs in the US.

Instead, Ant has focused its offshore ambitions on building its presence in the rest of Asia, where it is working with nine payments startups, including the owners of Paytm in India and GCash in the Philippines, targeting billions of people. It also seeks to link more overseas merchants to use Alipay, so that its Chinese customers can use it while traveling.

Controversies: Yahoo!

Jack Ma spun off Alipay from Alibaba into a company he controlled in 2011, citing the risks of having foreign ownership in the highly sensitive payment systems business due to its impact on financial stability and data collection. Yahoo! Inc. and SoftBank Corp. owned the majority of Alibaba at the time. Yahoo challenged the move, and ahead of Alibaba’s record $ 25 billion IPO in 2014, the companies reached an agreement that entitled Alibaba to a share of Ant’s profits.

That deal was terminated when Alibaba purchased a 33% stake in Ant in 2018. Ant now has other foreign investors, even Warburg Pincus LLC, Carlyle Group Inc. and Silver Lake Management LLC.

Ant shut down its Zhao Cai Bao platform after Cosun Group, a Chinese telecommunications company in Guangdong province, defaulted on bonds sold through the platform. When Zhao Cai Bao was the first Created, the vision was to create a platform that would allow small businesses and individuals to borrow directly from investors.

Future risks

Ant’s rise and dominance of China’s financial landscape has not gone unnoticed by the country’s regulators. An imminent threat is the Chinese central bank’s creation of a digital yuan, which is part of a push to control the stability of its payment system. Ant has faced regular scrutiny from authorities, looking at everything from his escrow service to loan risks.

Ant warned in his prospectus that growing trade tension between the United States and China could threaten his business as he prepares for the IPO. If the United States imposed certain sanctions, it could affect Ant’s business in Southeast Asia and India, for example.

In 2018, Ant’s attempt to acquire MoneyGram International Inc., a US-based remittance company, was unsuccessful. A change in foreign investment regulations in India led it this year to halt new investment in Zomato, a restaurant aggregator and food delivery startup.

| No. 1 and bigger | |

|---|---|

| The largest online consumer credit service | Huabei, Jiebei |

| The largest online investment services platform | Yu’ebao |

| The largest online insurance platform | Xianghubao, sale of insurance to third parties through Alipay |

| N ° 1 loan platform for small and medium-sized companies | My bank |

| The largest digital payment platform | Alipay |

| Note: Chinese market. All services can be accessed through Alipay | |

| Note: Ant owns a 30% stake in MYbank |

Who owns Ant?

The IPO is meant to make a lot of people very rich and Jack Ma even more. It owns 50.52% of the voting rights in Ant, through its control over the shares of Hangzhou Junhan and Hangzhou Junao. Ma has said that he intends to reduce his financial interest in Ant to no more than 8.8% in the future and is also donating 611 million shares to charity.

Others who are willing to pack a bundle include Ant Chairman Eric Jing and 17 other current and former Alibaba executives and Ant will join the ranks of the billionaires.

But the full scope of Ant’s backers is unclear, as Junhan and Junao do not disclose inclusive lists of people who receive financial interest through direct actions or representation contracts.

– With the help of Chloe Whiteaker