[ad_1]

Any strong economy reflects its robust financial system, so when macroeconomic indicators point in a positive direction, it is largely driven by financial sector players. Financial analysts and researchers were equally concerned about how the COVID-19 pandemic could derail the progress made in sustaining the banking sector during crises. Globally, to reduce the spread of the new COVID-19, governments enacted mitigation strategies based on social distancing, national quarantines and the closure of non-essential businesses. The stagnation of the economy had a major impact on the business sector, which had to struggle to find cash to cover operating costs as a result of the revenue shortfall. The financial sector, and commercial banks in particular, are expected to play a key role in absorbing the shock, providing much-needed funding (Acharya & Steffen, 2020; Borio, 2020).

Indeed, in these unprecedented circumstances, central banks and governments approved a wide range of policy interventions. While some measures have been aimed at reducing the strong tightening of short-term financial conditions, others have sought to support the flow of credit to companies, either through the direct intervention of credit markets (for example, credit lines sponsored by government and liability guarantees), or relax banks’ restrictions on the use of capital reserves. Although credit institutions were called upon to play an important countercyclical role in supporting the real sector, these actions also have a number of implications for the future resilience of the banking sector. For example, as lenders deplete their existing reserves, they may also experience deterioration in asset quality that can threaten the stability of systems. As the crisis is expected to continue, even after the locks were lifted and the economies began to reopen, the net effect of these policy measures on the banking sector is largely unknown. Ghana’s commercial banks recently released their 3rd management finances for the 2020 quarter and a quick review is underway to understand how they have managed to sustain shocks during this pandemic.

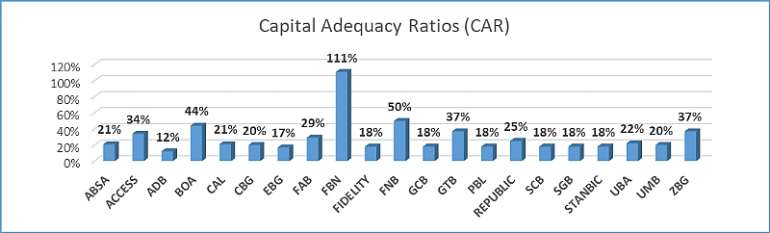

Capital adequacy levels

The capital adequacy ratio (CAR) is a measure of a bank’s available capital expressed as a percentage of a bank’s risk-weighted credit exposures. Basically, it is used to protect depositors and promote the stability and efficiency of financial systems around the world. But it is important to look at the two types of capital measures: Tier 1 capital, which measures how any bank absorbs losses without requiring a bank to stop operating, and Tier 2 capital, which can absorb losses in case of -up and provides a lower degree of protection to depositors. In my opinion, the Bank of Ghana looked to the future and asked the banks to raise capital from 120 to 400 million Ghs to ensure that the banks were stronger to withstand some of these shocks. Due to COVID 19, the Bank of Ghana lowered the CAR from the prudential limit from 13% to 11.5%. Despite the crises, all banks maintained a high level of capital well above the prudential limit to absorb shocks in case of uncertainty. Solvency continues to be strong with the industry CAR of 20.9% well above the regulatory minimum of 11.5% according to Basel II / III. Higher capital adequacy above the regulatory threshold indicates that banks have more scope to make loans.

Annex 1, Capital adequacy index of commercial banks as of September 2020

Annex 1, Capital adequacy index of commercial banks as of September 2020

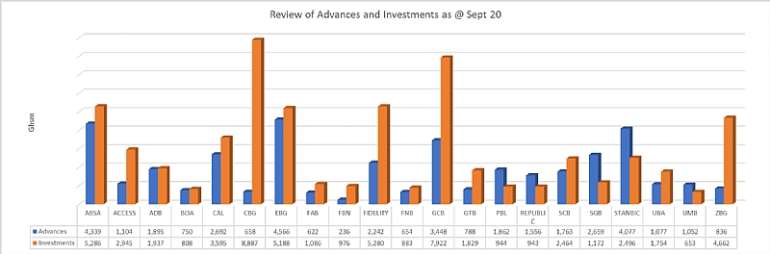

Asset quality

During this Covid -19 period, the general expectation was that commercial banks would be able to take a tight credit stance and reduce their loan portfolio. The reasons are that lockdowns and the general slowdown in the economy could result in cash flow challenges that could invariably lead to high levels of NPLs.

However, according to Bank of Ghana data, asset growth was even stronger and new advances have been increasing from the beginning of the year to date. Total bank assets increased 23.8% year-on-year to 142.6 billion Ghs, compared with growth of 10.1% a year earlier. The growth was generalized and was reflected in national and foreign assets, which increased by 24.5% and 15.6%, respectively. Relatively higher growth in domestic assets raised its share of total assets to 92.4%, down from 91.8% during the period. The main problem identified is that the majority of commercial banks continue to maintain important deposits in Investments that should go to the private sector to boost the economy. The recommendation to the Bank of Ghana is to limit the amount of investment banks can hold and instead deploy excess liquidity to improve the low Asset to Deposit ratios of some of the banks.

Annex II, Levels of advances and investments held by banks

Annex II, Levels of advances and investments held by banks

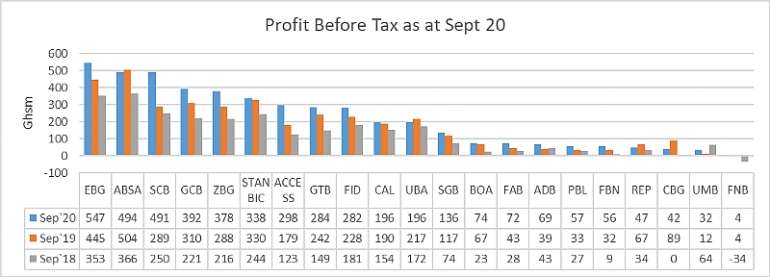

Profitability / earnings

Profitability indicators remained strong during this pandemic. Banks remained profitable despite COVID 19 and its associated challenges. As of September 20, industry revenues (excluding the National Investment Bank) increased 18% to Ghs10.8bn from a position of Ghs8.86bn in the same period last year. However, when you compare the industry growth of September 19 with that of September 18, the industry revenue increased 27%. GCB, Ecobank and Absa held market shares of 12.7%, 11.8% and 9.5%, respectively. Absa Bank (Ghs494m) lost its first place as the most profitable bank to Ecobank (Ghs547m) due to a 2% year-on-year decline. It is noteworthy that Standard Chartered (Ghs491m) went from sixth position to third position in Profit Before Tax (PBT) with a growth of more than 70% year over year. I think this is due to the bank’s strategic commitment to enhance its technological drive to serve its customers. Overall industry PBT increased 20% to 4.5 billion Ghs.

Exhibit 3, Profit before taxes as of September 2020

Exhibit 3, Profit before taxes as of September 2020

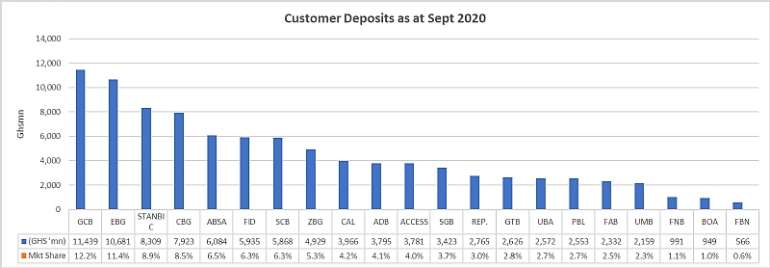

Liquidity levels

The banking sector remains liquid and well positioned to absorb liquidity shocks. The development reflects the benefits of recent banking sector reforms and COVID-19 policy responses. Therefore, the sector alone can correct these liquidity imbalances derived from mild to moderate shocks through interbank activities. During the lockdown, many transactions were conducted online, many banks revised their transactional charges, including mobile money charges intended to ease the suffering of customers.

Annex IV. Customer deposits for commercial banks as of September 2020

Annex IV. Customer deposits for commercial banks as of September 2020

Management team

The test of leadership has really been demonstrated during this period of COVID 19. In fact, during the period of lockdown, the crisis management team of several banks really proved that they were on top of the game seeking the well-being of their staff. To date, some banks still have a shift system and some have more than 70% of their staff still working from home. According to an article published by Bloomberg in 5th In November 2020, “ Stanchart introduces the permanent switch to flexible work from home 2021 ” and the report further indicated that approximately 90% of its 85,000 employees will have the option to choose the location, the hours. This is a sign of how the administration is dealing with pandemic crises. The leadership of some banks provided laptops, Internet services, travel packages, protective equipment and other security measures and equipment, etc. The administration also made some drastic decisions to improve technology and ensure stable systems. The list can go on and on, but the important thing is, all competing banks did very well to stop the spread of the virus to their staff.

To conclude, the spread of COVID-19 represents an unprecedented global impact, and the disease itself and mitigation efforts, such as social distancing measures and lockdowns, have a significant impact on economies globally. Commercial banks have lived up to expectations by playing an important role in absorbing the shock to the economy. There were expectations that commercial banks would have suffered the most during the COVID 19 period, however last quarter results have shown that banks remain resilient, well capitalized and with high liquidity buffers. I think the full year 2020 results will show an even more positive result.

Thank you for reading.

Credit: Daily Graphic, Business and Financial Times, Bank of Ghana, Banking Sector Report 20, World Bank, Miriam Amoako, Sophia Kafui Teye (Fidelity Bank Securities)

DisclaimerA: The points of view expressed are personal points of view and do not represent those of the media house or institution where the writer works. The analysis excludes the financial status of the National Investment Bank.

About the writer

Dr. Carl Odame-Gyenti, is a finance and telecommunications enthusiast, manages banks and non-bank financial institutions, local and global custodians, trustees, asset and pension managers, insurance and Fintech relationships with an international bank in Ghana . Contact: [email protected], Mobile: + 233-200301110