China is the first major economy to return to growth since the coronavirus pandemic

The Wall Street Journal reports that China is the first major economy to return to growth since the coronavirus pandemic.

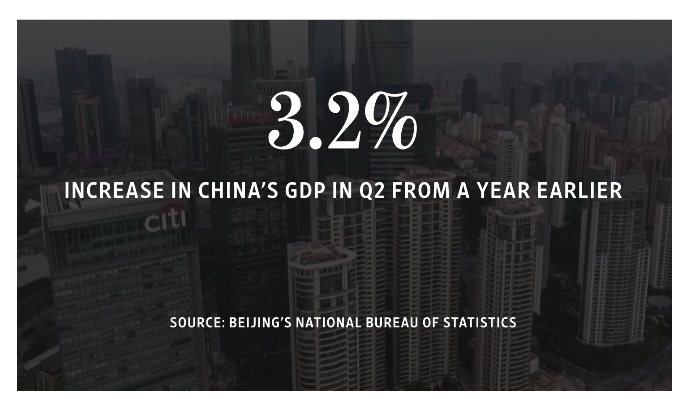

On Thursday, China said its economy grew 3.2% from a year earlier in the second quarter, as authorities benefited from an aggressive campaign to eradicate the virus within its borders.

In sequential terms, second-quarter growth in China’s gross domestic product accounted for an 11.5% rebound from the first three months of the year, according to data released by the Beijing National Bureau of Statistics. During the first six months of the year, China’s economy contracted just 1.6% compared to the first half of 2019. The growth figure for the second quarter exceeded an average estimate by economists for 2.6% growth and was at the high end of a An unusually wide range of forecasts, from a 3.1% contraction to 3.5% growth. A historic contraction of 6.8% followed in the first three months of the year, when Beijing closed the country in late January when the coronavirus spread across China from the central city of Wuhan.

It’s not what it seems

Michael Pettis at China Financial Markets has a different opinion in a Tweet thread.

- Markets drop sharply on China’s “unexpectedly” strong growth data today. Like many other analysts, I expected the data to exceed expectations, but the market reaction completely misled me.

- The fact that markets fell so fiercely on the “good” news may be important, perhaps marking a highly anticipated change in the way analysts interpret Chinese data. Rather than celebrating a strong recovery on the supply side, everyone seems to have focused on bad numbers on the demand side.

- Retail sales decreased 3.9% in the quarter. Real disposable income decreased 1.3%, and there is a lot of evidence that its decrease was distributed asymmetrically: the wealthiest households actually saw an increase in income, while for the rest, the poorer, the greater the decrease. .

- On the other hand, a top-tier European manufacturer told me today that while car sales in China have been stronger than expected, luxury car purchases have skyrocketed, perhaps reflecting a unique response to Covid-19. While cheaper car purchases have plummeted, it seems unlikely to return.

- Covid-19 is a shock on the demand side, and I think there is growing recognition that China’s wrong response on the supply side must mean a growing trade surplus (which we are already seeing and that is bad news for the rest of the world, assuming …

- … is allowed to continue) or a growing internal investment, which mainly means a non-productive investment and, consequently, an increase in debt.

- He was particularly intrigued by Jamil Anderlini’s statement (below) that “investment by private companies fell 7.3 percent.”

- This is very bad news. It means that the share of investment driven by state sector spending on non-productive infrastructure or investment in real estate development is increasing much faster than expected.

Behind the recovery, China’s economy falters

Item 7 above refers to the Financial Times article Behind the recovery, China’s economy is reeling.

China’s supposed solid recovery required a Herculean effort and more state debt, the same tools as ever. Anderlini reports that The investment of state-owned companies in the first half increased 2.1%, while the investment of private companies decreased 7.3%.

His conclusion is amusing.

- A decade ago, some economists liked to describe the Chinese economy as a bicycle that needed to maintain a certain speed or it would tip over and crash.

- Today it is more like a bicycle loaded with huge boxes of debt, ridden by a drunk and with strategic competitors like the United States trying to knock it down.

It is not just China. So let’s correct point 2 to be more precise.

The global economy is like a bicycle loaded with huge debt boxes run by drunken central bankers hoping to put more debt in the boxes despite the consequences of debt deflation from their stocks.

Mish